One of the diseases that afflicts communication is the desire to reduce every issue to its bare minimum, misinforming and creating two fronts of supporters. Just think of the NoVax versus SiVax issue, which also involved scientific luminaries, or the Ukraine issue. This way of dealing with complexity permeates not only the media, but also the halls where decisions are made – an even greater problem when the environment and the survival of life on the planet are at stake. In the case of the electric car (EV), there are those who argue that EVs will solve all CO2 problems, and those who believe that EVs will be the source of untold cataclysms.

The SiWatts accuse the some of being in the pay of the big oil tycoons, while the NoWatts accuse the others of being ignoramuses in the pay of governments. The suspicion is that there is a similar division in the European Parliament, and that certain irrational decisions are more the product of gurgling bellies than of thinking heads. Here we try, with prudence and love of detail, to put the pros and cons on the table, leaving it up to each reader to decide which way the scales should tip: in any case, synthesis is far from at hand.

Trying to reason about the facts, and the consequences of the decisions taken. If the European Union, for example, closes the roads to the combustion engine, does this mean that the heavy shipping, aviation and lorry traffic will stop at our borders and increase all around us? Will it mean that all our competitors will live in an oil economy, where we travel at rock-bottom prices, and that we will have to pay a huge surplus to deliver home what is only brought to us at the border? Or will we force poor countries to buy Teslas? And who will supply our cars with electricity as soon as they reach the Union’s borders? Is the West really rich enough to afford this?

The Brussels decision

8 June 2022: European Parliament approves end of combustion vehicles in 2035[1]

As part of the European Green Deal, with the Climate Act, the European Union, which is the third largest producer of greenhouse gases after China and the United States, has set itself the binding target of achieving climate neutrality by 2050, reducing greenhouse gases by 55 per cent by 2030: something that has become a real legal obligation for the entire Union. The package of proposals, called ‘Fit for 55’[2]. was adopted by the European Parliament on 8 June 2022 with 339 votes in favour, 249 against and 24 abstentions, and it concerns the revision of the CO2 emissions law[3].

The main directives are epoch-making, car manufacturers must reduce the average emissions of their entire fleet by 100 per cent from 2035, with intermediate measures in 2025 and 2030, and there is only one way to do this: the complete replacement of thermal propulsion with electric propulsion. This translates into a complete stop in the production of vehicles powered by petrol, diesel, LPG and hybrids. The internal combustion engine, patented in 1853 by the Italians Eugenio Barsanti and Felice Matteucci, is apparently destined to disappear. A frightening decision. Among the first to oppose it is Germany, which is withdrawing its support: its transport minister, Volker Wissing, is convinced that the best way forward is a holistic approach involving solutions on several fronts, especially that of synthetic e-fuels[4].

France is also opposed, preferring a ‘softer’ time target and defending plug-in hybrid engines[5]. In Italy, the Minister for Ecological Transition Roberto Cingolani expresses strong doubts about the choice for electric: accused by the Greens of wanting to ‘sabotage the ecological transition’[6], he is for a more cautious approach and the use of biofuels. Although ANFIA (Associazione Nazionale Filiera Industria Automobilistica[7]) speaks of the risk of losing 70,000 jobs[8], the Minister is convinced that these jobs will be reabsorbed by new professionalism and new services[9]. Italy, Portugal, Slovakia, Bulgaria and Romania demand a 90 per cent reduction of CO2 from cars by 2035 and a 100 per cent target by 2040: five years more time[10].

ACEA, the European association of car manufacturers, considers the EU decision to be ill-considered and is sceptical about the timing. Its position triggers illustrious defections, such as Volvo and Stellantis, which disagree with this view[11]. The Chinese Geely Auto Group has also decided to leave ACEA[12]. The ferment is enormous, not least because there are those who consider the transition to EVs inescapable and anticipate the timing: as early as 18 November 2020, Great Britain announced a ban on the sale of new petrol- and diesel-powered cars and vans by 2030, five years ahead of schedule[13].

This is a country that has been losing its car industry for decades. The Anglo-Saxons were the first of the G7 to set a legal target of zero emissions by 2050. The stop is also announced by California and Canada, but by 2035[14]. On 4 December 2020, Denmark declared its intention to increase the number of EVs and hybrids on the road from the current 20,000 to 775,000 cars by 2030 in order to reduce emissions by 70 per cent by 2030, but with the even more ambitious goal of hoping to reach the 1 million mark as soon as possible[15].

The electric vehicle market flies

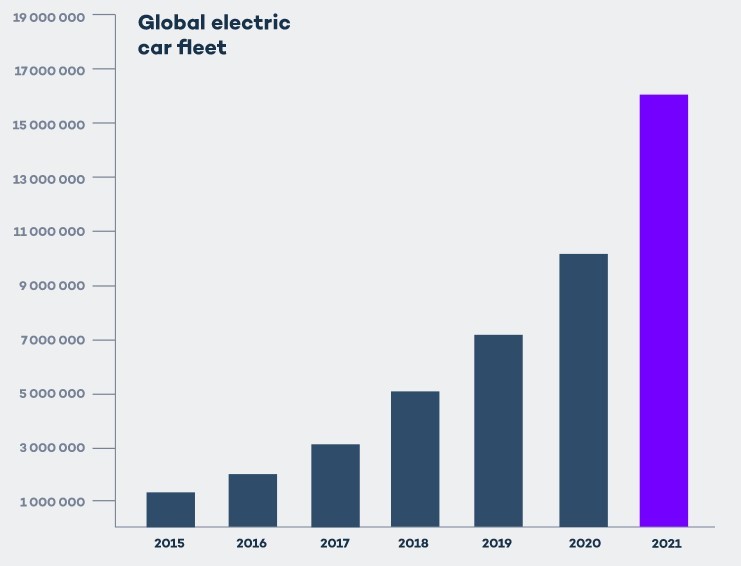

Total EVs sold worldwide per year[16]

The EV market is a vertiginously growing reality: despite the fact that 2020 was, due to the pandemic, a year to forget (for the entire automotive sector), EV sales compared to 2019 jumped 43%, and the EV industry’s global market share rose 4.6%[17] – a record. 2021, despite persistent chip shortages and rising prices of key raw materials, even saw a doubling of EVs: 6.75 million vehicles sold[18], and the year ended with a total of 16.5 million EVs circulating worldwide[19].

2022 is an even more exceptional year: 4.2 million EVs sold in the first half of the year, up 63% compared to the same period in 2021[20]; summary figures for June 2022 alone see 913,000 EVs sold, up 54% compared to June 2021[21], with a market share of 16% for June 2022 and 12% since the start of the year. The outlook is even more optimistic given the general political support for the entire sector worldwide: government spending on subsidies and incentives for EVs doubled in 2021 to almost USD 30 billion, and it is to be expected that the figures committed by governments in 2022 will be far higher[22].

China remains the largest market for EVs (more EVs were sold in China in 2021 – 3.3 million – than in the world as a whole in 2020[23]). Europe is catching up, driven by a strong emissions policy. In the United States, the market continues to be buoyed by the success of the Tesla Model Y: there is a strong general orientation of automakers towards EVs, with a focus on workhorse vehicles such as Ford’s F-150 and General Motors’ Silverado[24]. But EVs are more expensive than ICEVs (Internal Combustion Engine Vehicles), and China is trying to tackle this problem by producing small and affordable EVs (10% more than a conventional car on average). However, there are areas where buying an EV is still prohibitively expensive, such as Brazil, India and Indonesia (just 0.5% of the total car fleet), although India has managed to double its sales by 2021[25].

The pandemic and the war in Ukraine have dampened the market globally, but for the IEA’s 2022 Announced Pledges Scenario[26], which is based on climate-focused commitments and policy announcements, electric vehicles will account for more than 30% of vehicles sold globally by 2030. An impressive figure, but still well short of the 60 per cent share needed by then to achieve net zero CO2 emissions by 2050[27]. According to IEA estimates, EVs will reach just over 20% of sales in 2030[28]. The question is whether the Brussels directives are based on proper planning or whether, as the sceptics prophesy, we should expect a partial if not total failure of the targets. But the real question is: how strongly will these decisions affect the various social, political, industrial, geopolitical, economic and environmental spheres?

The electric car: why it is beneficial

An EV, compared to an ICEV, has fewer components and requires less maintenance[29]

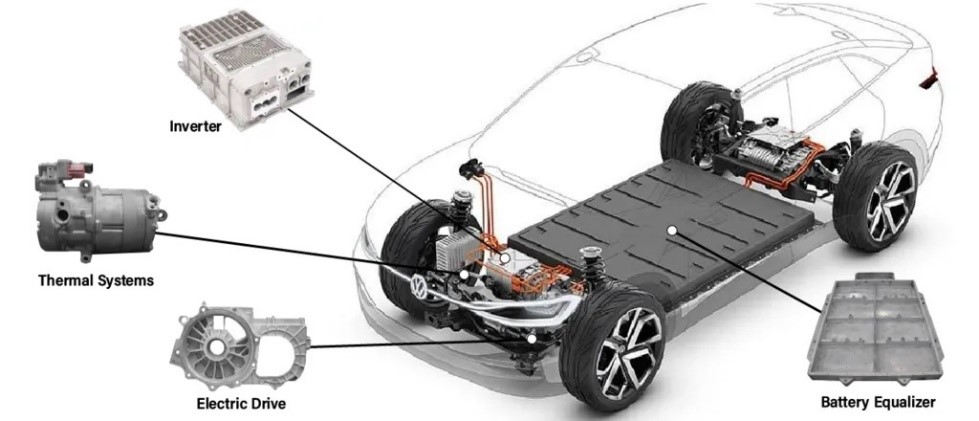

The main advantage is obviously the near-zero CO2 emission during operation. Another indisputable advantage is energy efficiency. In an ICEV only 30% of the energy moves the wheels: the rest is converted into heat, and is wasted. In EVs, on the other hand, you have efficiencies of over 80 per cent[30]. And there is the constructive simplicity: an EV is essentially composed of the battery pack, which is needed to store and supply the energy, the electric powertrain (which has a very simple structure), the inverter (the circuit that governs the powertrain), and the thermal system, which maintains the right temperatures in the engine and the passenger compartment. There is no gearbox, as speed and power are handled directly by the inverter, and many other mechanical parts are missing. What remains are the axles, wheels, differential, suspension, brakes, lighting.

The simplicity translates into huge advantages, both in reliability and maintenance costs. The braking system is the only one that shows some wear and tear, but it is considerably reduced compared to ICEVs: to brake, an EV uses the same motor and, in this phase, uses the force of inertia to recharge the batteries, thus recovering energy that in ICEVs is wasted. The rest of the components can be imagined to last the full life cycle of the car. The reduced use of components also has another positive consequence: increased cargo space. Even EVs with a very small volume offer larger luggage compartments than ICEV.

Another advantage is the ability to achieve maximum torque at very low engine speeds: ‘engine torque’ is the power that the engine is able to deliver in terms of thrust at low and medium engine speeds. An internal combustion engine has the characteristic of developing its power best from a certain number of revs upwards. This is not true with electric motors, which are able to release maximum thrust even at close to zero revs[31]. In terms of performance, this is a considerable advantage: no ICEV achieves the brilliant performance of an EV. Another plus point is the quietness, which is far less than with an ICEV.

The controversial aspects

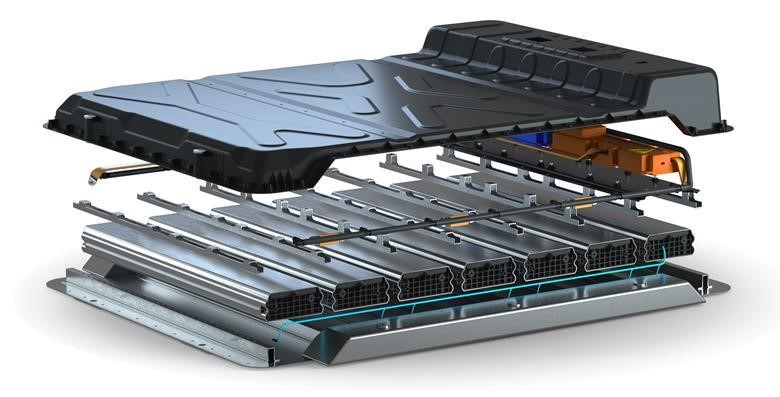

The lithium battery is the most controversial piece in terms of cost, safety, range, weight and pollution[32]

An important premise: we are in the technological sphere, changes can be very rapid and unpredictable, because as early as tomorrow a new discovery could revolutionise the electric car as it is today. The battery pack, which is the fulcrum around which the entire vehicle revolves, is also the one that touches the most sensitive aspects: cost, weight, recharging, autonomy, life cycle and safety. Other aspects, such as battery production and disposal, we will deal with in a later section: here we confine ourselves to issues purely confined to the use and maintenance of the vehicle.

Cost: this is what has the greatest bearing on the final price of the vehicle. Batteries are usually not produced directly by the car manufacturer, but are purchased from external suppliers, which makes their cost similar for everyone. According to Cairn Energy, Tesla pays an average of $142 per kilowatt-hour (kWh) for battery cells purchased from its three suppliers: Panasonic, LG Chem and CATL. In comparison, GM pays an average of $169 per kWh for its battery cells, while the industry average is about $186 per kWh. Cairn’s data estimates that Tesla’s battery packs cost, on average, $187 per kWh, while GM’s packs cost $207 per kWh; the automotive industry spends an average of $246 per kWh for battery packs[33]. The centrality of this component is, however, leading car manufacturers to take a less passive role and invest themselves in battery design and production[34].

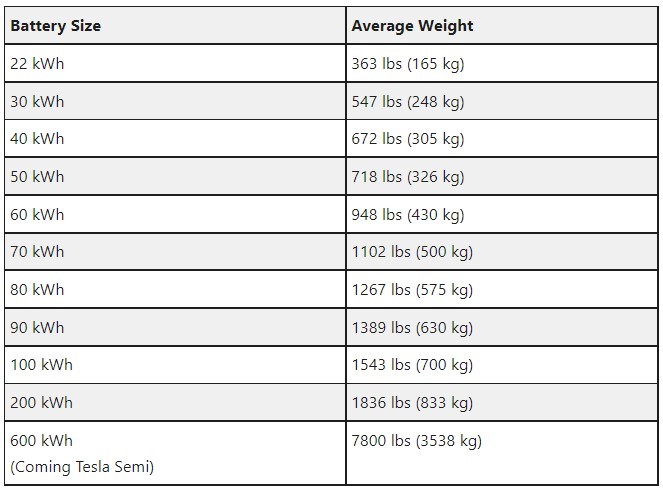

Weight: this is a crucial aspect, since in order to achieve a range that gives sufficient versatility to the EV, a significant weight is reached – currently between 600 kg and 1400 kg, but there are vehicles such as the Tesla Semi truck which exceed 3500 kg. The considerable weight negatively affects driving agility – although it has to be said that the battery pack, being in the lowest part of the car, lowers the centre of gravity and thus increases stability – and affects fuel consumption. It’s a dog biting its own tail: greater weight equals greater accumulation and thus greater range, but at the same time the greater weight negatively affects range. This is why the search for a good compromise is the aspect in which car manufacturers concentrate the greatest efforts.

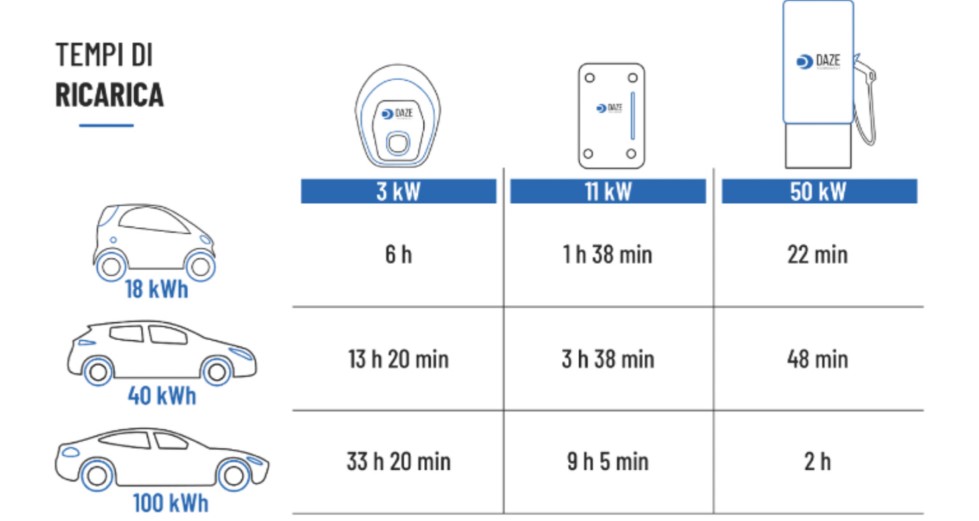

Time, charging mode and energy requirements. This is one of the elements that acts most as a brake when buying an EV: filling up with petrol takes three or four minutes, filling up with ‘electrons’ can range from 30 minutes to several hours. A typical EV with a fully discharged 60 kWh battery takes just under eight hours to fully charge with a 7 kW charging point, while a Tesla Model S could take as much as 21 hours with a 3.7 kW charging point[35]. Charging stations usually have the ability to deliver power in different modes, slow, fast and rapid (compatible with EVs’ charging systems), and this has a significant impact on charging times. However, using very fast recharging is tantamount to generating a considerable current, which will eventually increase the temperature of the batteries considerably and accelerate their degradation[36].

Weight of batteries in relation to power supplied[37]

To understand the charging process, a few aspects need to be specified. The first is the capacity of the battery, i.e. how much electrical energy it can store. This is measured in kilowatt-hours (kWh). The more kWh a battery has, the more energy it can hold (and thus the more kilometres the car can travel on a full tank). The second aspect is the charging power (or speed): this is the measure of actual energy over time that is transferred from the charging station to the car battery.

Ideally, this should be equal to the power of the charging station, but in reality it is limited by a number of factors, including: a) the power of the charging station, i.e. how many kW per minute enter the car battery. For example, a 22 kW wall box installed in a house where the maximum power availability is 3 kW, that will be the real limit of the charging power; b) the maximum charging power of the car – often lower than the power of the charging station; c) attaching one’s own charging cable to a charging station may limit the maximum current allowed by the cable. Cables that can carry higher currents cost more; d) especially in a domestic environment, charging stations are connected to networks with limited power availability and are therefore slowed down so as not to cause blackouts.

To calculate how long it takes to ‘fill up’, simply apply the following formula:

The result of this calculation is the number of hours required to charge the car battery (from fully discharged to fully charged). Here are some examples:

Recharge time of the machine battery from fully discharged to fully charged[38]

That said, if we assume an average consumption of 15 kWh per 100 km, at 3 kW charging power it takes about 5 hours to provide enough charge to cover 100 km, while it takes about 2 hours at 7 kW and about 40 minutes at 22 kW. The most common AC columns reach up to 22 kW in three-phase, while 7.4 kW is the upper limit for single-phase – a fundamental aspect when dealing with the rewiring of urban networks, which cannot ignore the fact that the stations that allow the highest charging speeds are DC-Direct Current stations (which are also the most technically complex and the most expensive) [39].

To connect to the charging station you need the CCS Type 2 cable (the most common European standard for so-called ‘slow’ charging, i.e. in alternating current, up to speeds between 40 and 50 kW) and the power varies depending on the model and the service provider: ENEL X allows charging at 50/100 kW, Tesla up to 250 kW and Ionity up to 350 kW[40]. Not all cars support all DC charging powers. The maximum value indicated by the car always applies. So, for example, a Kona Electric recharges at a maximum of 70 kW even at a 350 kW Ionity station[41]. When it comes to ‘fast’ charging, consider that a Tesla Model 3 takes about half an hour with Supercharger V3 and a Hyundai Kona Electric just under an hour with Enel X or similar)[42].

Other examples, based on the kilometres to be covered: a) to recharge 50 km, taking as a reference a consumption of 15 kWh per 100 km, with a charging power of 2.3 kW it takes just over 3 hours; b) using AC stations one can recharge up to 100 km in less than an hour, with cars equipped with a three-phase 22 kW charger; c) a DC fast station, as mentioned, can recharge 50 km in a very short but highly variable time; d) with a Tesla Model 3 Long Range charged at Supercharger V3 one can go down to 5/6 minutes[43]. This case, however, requires a 1 MW power cabinet that delivers 250 kW per vehicle. A truly difficult power load to handle.

So, regardless of battery technology and charging systems (which will undoubtedly offer better performance in 10 years’ time), the issue is that the shorter the charging time, the more instantaneous power must be supplied to the EV. The problem of energy requirements is not even alleviated by the continual launch of new solutions and/or technological features, such as the On-Route Battery Warmup, which enables the battery to be pre-heated so that, upon arrival at the Supercharger, the accumulator is at the ideal temperature for charging: a solution that may reduce charging times by 25%, but does not reduce the power required for charging[44].

Autonomy and spread of charging points

Current number of public charging points per European country in relation to vehicles on the road[45]

The range is related to the efficiency of the car: for example, a Mercedes 2022 EQS 450+ travels about 395 miles on a full charge, while an Audi e-tron Quattro achieves 188 miles of range[46]. These figures are highly indicative, as they depend on numerous variables such as load, driving style, topography, outside temperature, tyre type, use of heating, air conditioning or other devices in addition to normal absorption – and finally the age of the batteries[47].

If we compare the general autonomy of an EV to that of an ICEV, it is still considerably lower: the EV therefore ends up being preferred by those who need to make small journeys, but discourages those who want to make long journeys. Especially for the latter, another disadvantage looms large: the scarcity of charging points, which generates the inevitable ‘range anxiety’. There are usually different locations for so-called recharging stations, such as at home, in workplaces or in public areas, and the percentage of use varies from country to country – in addition to differences in habits and lifestyles, there are also large infrastructure gaps. The choice of where to place a post is linked to specific elements. For example, contrary to the rest of Europe, Finland and Sweden prefer residential stations[48].

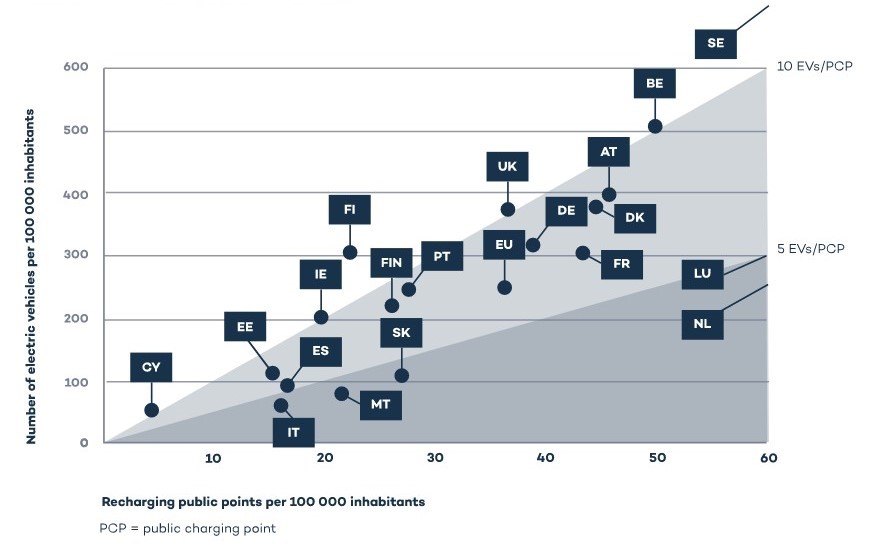

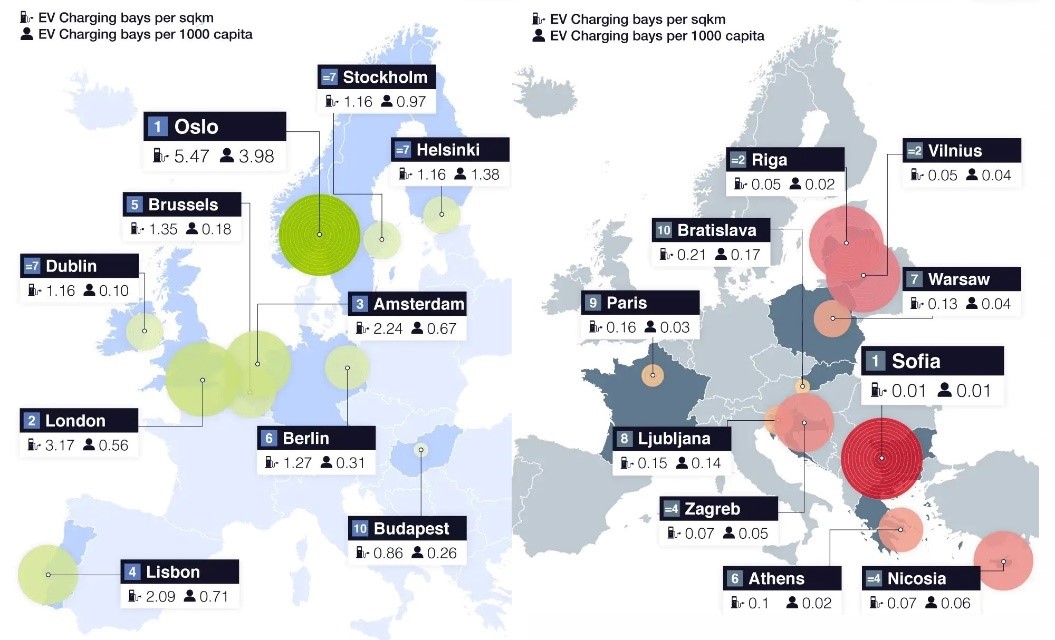

The situation with regard to the number of recharging points is not even sufficient today for the EVs currently on the road, which are also growing rapidly: there are around 330,000 recharging points in the European Union[49], but their irregular deployment does not allow for peaceful travel. Germany, France and the Netherlands have 69% of all charging points in the EU, while 10 European countries (such as Italy) do not even have one charger per 100 km of road[50]. The European Commission has set a target of 1 million charging points by 2025, predicting a frantic race against time. According to Uswitch research, the gap in the distribution of charging stations between European capitals is enormous: it ranges from the virtuous Oslo with 5.47 stations per km2 or 3.98 per 1,000 inhabitants, to the lousy Sofia with 0.01 stations per km2, 15 in the whole city[51].

On average, energy management companies have an optimistic attitude, and believe that the timeframe for upgrading will allow for the construction of an adequate and efficient network[52] – even though there are profound regional differences, and each country will have different access possibilities. Suffice it to say that the EU reached the target of 22% of energy produced from renewable sources in 2020 (it plans to reach 63% by 2030[53]), but if we look at individual countries we find Iceland with 83.7%, while Malta is only at 10.7%[54].

The Italian case: by 2030, decarbonisation targets envisage a fleet of 6 million electric vehicles (BEVs + Plug-in Hybrids) on the roads, with only 24,000 recharging points, most of which are AC, with power ratings of up to 22 kW, and mostly concentrated in the north. According to the estimates underlying the PNRR, by 2030 Italy needs 3.4 million recharging points (private and public), of which 32,000 are ultra-fast public points. The Motus-E association (which includes car manufacturers, energy and service providers and recharging station operators) has drawn up a scenario that envisages a network of 98,000 public recharging points by 2030 – for which the PNRR has earmarked just over EUR 740 million to upgrade the recharging network for electric vehicles[55]. Obviously: a German or a Finn, used to encountering a charging station every 5 km, would not choose a tourist destination where they risk being stranded without a recharge.

Comparing the best with the worst cities in Europe for the presence of charging stations (Uswitch report)[56]

The plan, again in Italy, envisages the construction of 7,500 recharging stations on motorways and motorways of at least 175 kW by 2026, and 13,000 stations of at least 90 kW in cities. According to Motus-E, including the impulse given by the PNRR investments, by 2030 there could be 108,000 charging points, with a mix of 51% fast and ultra fast (>50 kW) and 49% quick (22 kW) points. This includes about 2000 ultra fast charging points on the motorway network, with one charging station every 25 km, each consisting (on average) of 3 charging stations for a total of 6 charging points, with an average power of 130 kW’[57].

The current reality of ICEVs is that we have a widespread presence of diesel, petrol and LPG stations throughout the territory, with very short refuelling times. In the case of EVs, there is a lack of recharging areas, and refuelling times range from a quarter of an hour (very rarely) to several hours, depending on the power output of the point and the recharging modes supported by the vehicle[58]. Not only that: what does it mean to increase the number of recharging points so that everyone can recharge as they do today with hydrocarbons? Let us try to give an answer.

Charging stations will have a significant impact on the average consumption of any city, which does not have a sufficiently dimensioned electricity grid: for EVs, we will need to multiply electricity production. This will require a considerable adjustment effort, with structural rethinking and major investments. A key factor is energy, which, to achieve climate neutrality, will necessarily have to be produced from renewable sources.

This requires a profound rethinking of current structures, such as the spread of hybrid (solar/wind) autonomous energy generation points where possible: but is it realistic to be able to achieve all this in just a few years? And what percentage of the planet’s territory must necessarily be covered by photovoltaic panels and wind turbines to be able to do this? In today’s situation we would have to build dozens and dozens of new power plants fuelled by oil or gas, or coal. If we decided to build a nuclear power plant today, it could be in operation, if all goes well, in 15 to 20 years.

The subject is a very sensitive one. If we consider that one of the most debated ways of coping with the inevitable difficulty of recharging, given the current scarcity of public columns and the time needed to refuel, is to move increasingly towards domestic recharging points to take advantage of night time – also because of the lower cost of energy compared to public energy – or towards places of employment to take advantage of ‘dead’ time during work, or in large shopping centres, a Pandora’s box is then opened.

Italy: the PNRR devotes just over €740 million to upgrading the supply network[59]

In a household, an average of 3kW (+/- 10%) of power is available: considering that in a flat there are devices such as fridges, freezers, boilers, lighting, etc. in operation at night, which use more than 30% of the available power, one ends up dedicating about 2 kW to recharging an EV (and we are in any case at risk of a blackout): a totally insufficient power to cope with the traffic needs of even a small EV, which can recharge, at best, just over 10 km of range in an hour.

Are we all forcing everyone to resort to increased domestic power, resulting in higher bills? How much will these aggravations be offset by petrol savings? The risk is that this Green Revolution will present costs that will fall on households to an extent that is not easily foreseeable, even less quantifiable, and worse, unsustainable.

Reasoning on an average power requirement of just enough, this is around 75 kW per charging point. Within a typical city block of 10 flats and 30 people, at least 15 cars (a situation assumed downwards, since the Italian average is one car for every 1.65 inhabitants[60]), the results are heavy. Let’s try to think of the same installations in working areas, such as large offices or factories, which can hold hundreds of people with hundreds of cars: the problems to be solved from an infrastructural point of view are eschatological.

For public petrol stations, we obviously have to think in very different magnitudes: given the recharging times, a station would have to have at least three times as many recharging points as the current fuel pumps, up to probably 15 to 20 more than the current ones, in order to guarantee a good service. It must also guarantee a good power output per point, ranging from at least 100 to 350 kW, and its value will be directly proportional to the prestige of the service station.

There are currently 37 million cars on the road in Italy[61]: let’s imagine that they will be completely replaced by EVs; let’s also assume that, given the tight schedule, at least 30% of them will be refuelled at night, absorbing an average power per point of 74kW. The orders of magnitude leave no room for easy solutions: the entire country would immediately go into blackout.

To generate the electricity needed to replace petrol with green energy would require covering most of every available surface area on the planet with solar panels[62]

Charging EVs will be increasingly energy intensive. In order to satisfy the desire for short dwell times when charging away from home or the workplace, recent research funded by the US Department of Energy (DOE) aims to reduce typical charging time as soon as possible by increasing power levels up to 400 kW, and original equipment manufacturers (OEMs) are producing vehicles that can accept higher power levels, including the Tesla Model 3 (which accepts 250 kW as seen) and the Porsche Taycan (which accepts 350 kW). Fast charging networks, including Electrify America and EVgo, have both deployed 350 kW chargers and the new ChargePoint technology can deliver up to 500 kW[63]. Very expensive cars that would undermine the end of freedom of mobility as we know it today.

In a 2021 article entitled ‘Impact of Electric Vehicle Charging on the Electricity Demand of Commercial Buildings’, authors Madeline Gilleran, Eric Bonnema, Jason Woods, Partha Mishraa, Ian Doebber, Chad Hunter, Matt Mitchell, and Margaret Mann examine several studies assessing the impact of electric vehicle charging stations on the grid by examining numerous station sizes, charging power levels, and usage factors in various climate zones and seasons[64]. The conclusions reveal that an electric vehicle charging station has the potential to make a large building’s electricity demand pale into insignificance if it gravitates to the same meter, increasing the monthly peak demand for electricity by up to more than 250%[65].

Considering more generally the impact in agglomerations of a few million inhabitants, it is not difficult to guess that the widespread distribution will impose a rewiring of the entire urban and extra-urban electricity grid, the downsizing of the cables used, and the consideration of the increase in urban electromagnetic pollution due to the intense currents required (as well as decades of work).

Electromagnetic pollution

In Australia, the majority of charging stations are out of service: the grid has no electricity to support them[66]

A study in the journal Bioelectromagnetics compared the levels of low-frequency magnetic fields (range of 40 Hz -1 kHz) emitted by electric and petrol-powered vehicles to see whether the parameters measured were below the legal limits set out in the ICNIRP (International Commission on Non-Ionizing Radiation Protection) Guidelines, using 14 vehicles as a sample: 6 petrol, 5 electric and 3 hybrid cars[67]. The results are encouraging: the average magnetic field measured on electric cars is of the order of 0.095 mT compared to an average level of 0.051 mT measured on petrol cars. Much higher values have been measured on trucks (0.146 mT for electrically-powered trucks, 0.081 mT for petrol-powered trucks), but these values are still well below the reference levels for public exposure specified by law[68].

Concerns about EMF emissions from EVs are, however, related to the indirect effects of their deployment. As is well known, the impact of intense magnetic fields on health is a controversial issue[69]: it is no coincidence that the WHO, the World Health Organisation, has called electrosmog ‘the pollution of the 2000s’[70]. Numerous studies, including those conducted in 2000 by the medical faculty of the University of Bristol, that in 2017 by the Veronesi Foundation, and that of Alessandro Miani (President of SIMA Italian Society of Environmental Medicine) have produced controversial results on the pathogenicity (carcinogenicity hypothesis among all) of magnetic fields, but there is broad agreement on the interference on the human body and therefore on their potential danger[71].

In Italy, this uncertainty led, for the purpose of protecting the population from exposure to electric and magnetic fields, to the Decree of 8 July 2003, which set exposure limits for electric (5kV/m) and magnetic (100 mT) fields to protect against possible short-term effects. Attention values (10 mT) and the quality objective (3 mT) of the magnetic field were also established for protection against possible long-term effects in children’s play areas, living environments, school environments and places where people spend no less than four hours a day[72].

If the entire distribution will have to be redesigned to withstand considerably higher powers than at present, this will result in enormous electromagnetic emissions, the magnitude of which is difficult to predict, especially in urban areas. At this point, one wonders whether, in the EU, anyone has had the slightest inkling of the orders of magnitude that such a choice might have generated – or whether anyone has at least asked themselves the question. As we write, there does not seem to be any reference to this.

The life of a battery. With the purchase of the first EVs, there was a real fear that sooner or later they would have to face a significant battery replacement cost. This is no longer so true, as there are now batteries with a life cycle of more than 10 years: it is true that the loss of efficiency due to use is progressive, but it is still negligible[73]. A federal law in the US stipulates that the batteries in an EV must last at least eight years (or 160,000 km), otherwise the EV manufacturer is obliged to cover the warranty, but all manufacturers now protect their customers using similar parameters. The replacement cost, depending on the model, can be around $100/130 per kWh (prices fluctuate greatly)[74]. Adding the labour cost, the expense becomes very significant: it could be around $12-20,000 for a battery of less than 50 kWh in vehicles such as the MG ZS EV, BMW i3, Nissan LEAF and MINI Cooper SE, and up to $50,000 in long-range prestige vehicles such as the Porsche Taycan, Tesla Model S, Mercedes-Benz EQC and Audi e-tron[75].

A Volkswagen ID3 bursting into flames after being disconnected from charging[76]

The fire risk of lithium batteries. This is a sore point that ‘ignites’ minds: what is the real fire and explosion risk of batteries? Today, lithium-ion cells based on graphite anodes and layered oxide cathodes (NMC, LMO, LFP)[77] are used, which have among their greatest advantages over other battery types a great capacity to store energy and extract it quickly. The weak point, in terms of safety, is the use of the liquid electrolyte based on organic carbonates[78], which, when subjected to thermal stress, can ignite very quickly – resulting in a risk of explosion and the emission of highly toxic hydrofluoric acid gas.

An EV battery fire would seem to be a catastrophic event (according to some, well above a petrol or diesel tank fire, according to others, exactly the opposite, which certifies the chaos in the interpretation of the little data available and perhaps, in some cases, bad faith) for three main reasons: a) the rapidity and violence of combustion can prevent the timely evacuation of passengers, the explosion has even more damaging effects. The batteries occupy the entire bottom of the car, a position that puts passengers at great risk[79]; b) the type of materials and their behaviour during combustion make it difficult (if not impossible) to extinguish quickly: it usually takes several hours and, even when the fire has been put out, there is the possibility of a reignition, even after some time, with the risk of fire expansion (the case of firemen having to throw a Tesla into the water because they cannot extinguish it has set the standard[80]); c) the circulation of high electrical voltages inside the EV (even 800V) obliges great care when extinguishing fires: the use of liquids, for example, exposes firefighters and occupants to deleterious electric shocks; d) during combustion, abundant highly toxic hydrofluoric acid and phosphoryl fluoride gas is emitted[81], with serious damage to the environment and those present: woe betide if the fire occurs in crowded places or indoor car parks.

This should not make us irrational: estimating the real risk requires us to compare models based on experience and not perception. We are still at an immature stage for valid answers. But the risk is real: Tesla confirms as many as 97 cases of fire to date that have claimed 38 lives: half of the fires are indicated as spontaneous, the other half as the result of accidents, some of them even minor, but which nonetheless triggered combustion[82].

Several car manufacturers have recalled their cars because of the fire risk, with very serious costs: between 2020 and 2021 General Motors’ Bolt will suffer damages of USD 1.9 billion thanks to two manufacturing defects in the cells supplied by LG Chem, which have set at least 13 vehicles on fire[83]; Hyundai will lose USD 900 million, forced to replace the defective batteries in at least 82,000 Kona Electric cars after several fires[84]; the recall of 33,000 Kuga plug-in hybrids will cost Ford USD 400 million – again because of fires caused by defective batteries[85]. BMW also announces a serious problem on its plug-in hybrid line: the recall affects 26,700 vehicles worldwide, all of them at risk of fire[86].

The news unfortunately reports numerous disasters caused by the combustion of EVs, such as collapsing car parks, cargo ships carrying fleets of EVs catching fire and sinking[87] (the Sincerity Ace in 2018[88] and the Felicity Ace in 2022[89]), as well as countless EVs incinerated due to accidents or spontaneous combustion. NTSB research states that after 41 fatal crashes involving EVs, only one caught fire (2.44%); after 20,315 fatal crashes involving petrol-powered vehicles, 644 caught fire (3.17%); after 543 fatal crashes involving petrol-powered hybrid vehicles, 12 caught fire (2.21%)[90]. From this data, it would appear that EVs are safer than ICEVs, but Graham Conway, an engineer at the Southwest Research Institute in San Antonio, Texas, disputes the finding, as the calculation is flawed by the huge sample size gap between EVs and ICEVs, and is therefore not statistically representative[91].

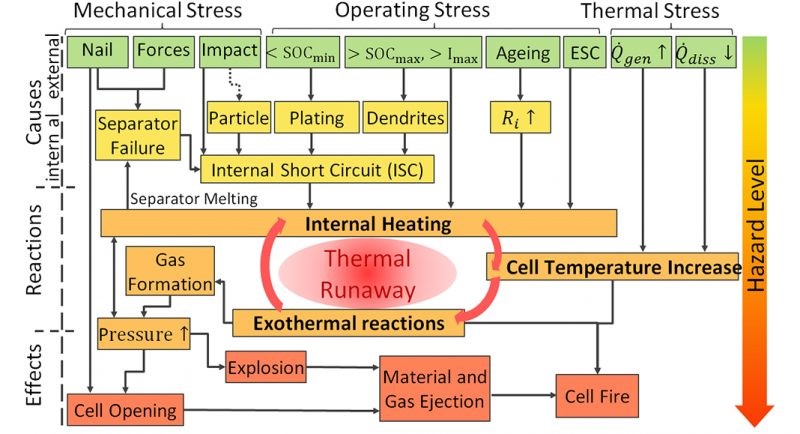

Causes and effects of thermal instability in lithium ion cells during normal use, abuse or accidents[92]

There are numerous studies and statistical surveys on the subject, but it is complicated to arrive at an objective synthesis, since the results are conflicting due to the small number of EVs in circulation compared to ICEVs, which does not yet allow for a proper statistical comparison, and due (very disturbing) to the staggering interests that revolve around mobility, so it is likely that some studies present ‘tame’ results. The technically incontrovertible fact is that today’s lithium batteries can catch fire and explode due to the excessive temperature that can develop inside the batteries under abnormal conditions.

At the root may be manufacturing or design defects, abnormal or improper use, an improper or defective charger, low-quality components, a short circuit, external stresses such as shock or pressure. In anticipation of this very real risk, increasingly sophisticated and efficient devices have been incorporated that attempt to limit the risk of triggering or the resulting damage – such as sensors that monitor temperatures, or cell separation systems that deactivate cells in the event of criticality. The entire set of batteries is encapsulated in protection from external agents[93], protecting them from mechanical stresses which, as we have seen, are a high cause of risk, and containing the development of flames and deflagration as far as possible[94].

The danger is therefore real, but it is legitimate to think that we are in a transitional phase and that things will improve: manufacturers are busy looking for safer solutions. There is in fact great ferment in the engineering of batteries: batteries are being studied which, in addition to having greater storage capacity and being able to be recharged more quickly, also have a significantly reduced risk of fire and explosion, using a polymer or even ceramic electrolyte, no longer liquid[95]. We can therefore safely assume an imminent future in which we no longer have to worry about this.

The environmental impact

In many countries of the world, people work in mines without any respect for human rights and the environment[96]

The debate on the real green role of EVs is open: their low CO2 emissions, as well as other pollutants, during their operational phase is indisputable. But a serious analysis must take into account the total cycle of an EV, from the sourcing of the raw materials necessary for its production to its disposal at the end of its life; the impact arising from the use of millions of tonnes of copper, steel and rare earths for millions of columns must be considered, and if we look at electromagnetic pollution, we are no longer talking about a product with a virtuous cycle. Here we enter a very complex field because there are so many elements to consider.

Raw materials. Although EVs require fewer materials than ICEVs (such as steel, aluminium and copper), the demand for minerals is six times higher[97]: lithium, cobalt, graphite, terbium, dysprosium, neodymium, for which procurement is complex and polluting. According to the US Department of Energy Argonne National Laboratory, a single lithium-ion car battery (of the type known as NMC532) contains about 8 kg of lithium, 35 kg of nickel, 20 kg of manganese and 14 kg of cobalt[98] and, given the rapidly increasing diffusion, the availability of huge quantities of these elements is crucial for the manufacturing industry.

The availability of lithium in nature does not seem to be a cause for concern: the US Geological Survey estimates that the current reserves – 21 million tonnes – are sufficient to carry the conversion to EVs into the middle of the century[99]. The situation for cobalt is different: two-thirds of the global supply comes from the Democratic Republic of Congo (with China controlling at least 70% of the mining in DRC[100] and currently undergoing a major expansion into territories such as Cameroon, Angola, Tanzania, Zambia and Greenland[101]), in mines that violate human rights[102] and environmental respect[103]: first and foremost the multinationals Glencore Plc, China Molybdenum, Fleurette, Vale and Gécamines[104].

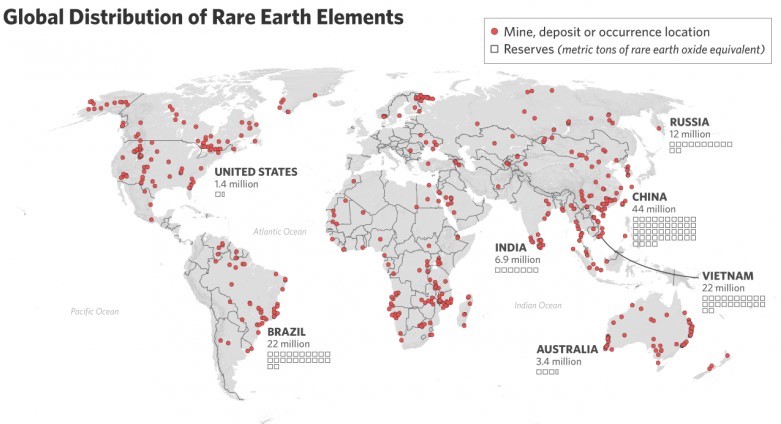

In 1987, Chinese President Deng Xiaoping said: ‘The Middle East has oil. China has rare earths’. Almost 40 years later, China is still the absolute protagonist: 168,000 tonnes in 2021, followed by the United States with 43,000 tonnes and Myanmar with 26,000[105]. When it comes to reserves, China remains at the top with 44 million tonnes, followed by Vietnam with 22 million tonnes, then Brazil on a par with Russia with 21 million tonnes – a total of 120 million tonnes[106].

In lithium mining, what is of greatest concern is the environmental issue: current mining methods require huge amounts of energy (for lithium extracted from rock) and water (for extraction from brines), although more modern techniques use geothermal energy, which is considered to be less worse. Nickel is not enough, but thanks to technology, less and less will be used in the future[107].

Map of rare earth production and distribution of reserves[108]

Rights and environmental violations related to rare earth mining are also widespread in other countries, such as China, where the ecosystem of vast territories has been irreparably destroyed[109]. Rare earths, contrary to what their name suggests, are very abundant in nature: their name derives from the fact that they are found in low concentrations – and when they are found, they are difficult to separate from other elements, so highly polluting systems are used.

Mining consumes huge amounts of fresh water and pollutes soil, groundwater and air. Vast open-pit mines cause deforestation and threaten biodiversity[110]. Extraction, processing and transport of minerals consume huge amounts of energy, generating greenhouse gas emissions. Rare earths themselves become pollutants when released into the environment in the form of emissions or waste. It is very difficult to intervene with environmental audits in often hostile countries. There is also, in many places, illegal mining that eludes all rules, and is the most damaging[111].

In short, if you have been told that EVs are magic vehicles… well, that is not really the case. But their compulsory introduction will cause a substantial decrease or, in the future, the complete elimination of the use of fossil fuels: the savings in pollutant emissions will perhaps compensate for the failures they bring with them. The impression, however, is that the transition will take longer than planned. Unless oil is used, instead of in the tanks of cars, in those of the power stations that have to produce the electricity needed to run the EV.

The geopolitical issues

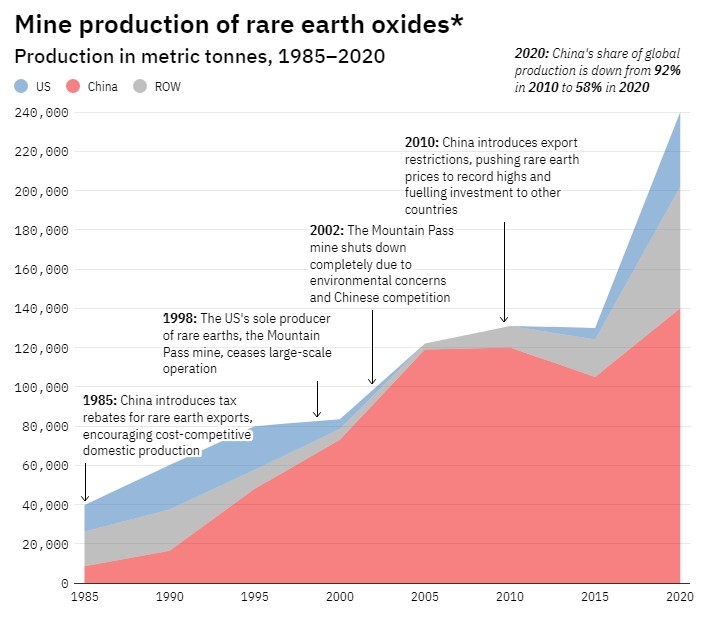

Rare earth mining production between 1985 and 2020[112]

The possession of rare earths in high concentrations in the hands of a few obviously poses a serious question about their redistribution. If these few are represented by countries with which, historically, one has ‘complicated’ relations, the question becomes serious. Soon the demand for rare earths will undergo a boom that will go hand in hand with the sharp increase in EV production and the revival of renewable energy production[113]: 2 tonnes of neodymium[114], 335 tonnes of steel, 4.7 tonnes of copper, 1200 tonnes of cement and 3 tonnes of aluminium[115] are used in a 3MW wind turbine. Adamas Intelligence[116] predicts that the market for magnetic rare earth oxides will grow fivefold, from $2.98 billion in 2021 to $15.65 billion in 2030[117].

According to the International Renewable Energy Agency, to achieve net zero emissions by mid-century, the global cumulative installed capacity of wind power must triple by 2030 (to 1,787 GW) and increase by 900% by 2050 (to 5,044 GW) compared to the installed capacity in 2018 (542 GW). China is the country with the greatest capacity to meet demand, as it holds the largest share of reserves, as well as being the largest producer[118]. This implies that the United States and the European Union will have a dependency role (only 3% of the raw materials needed for lithium batteries are extracted in Europe[119]), as has been the case for decades for oil. This affects the entire supply chain, from extraction to sale to consumers.

Rare earths are strategic in the military field, as they are essential for modern defence systems: the boom in demand in the civil field that could generate a rarefaction of supply would jeopardise supplies in this sector in particular – a risk that no western country is willing to take. Trying other avenues is not easy: Washington has only one rare earth mine, near the Mojave National Preserve in Mountain Pass, California, but it has a history of complex controversies. Having become inactive in 2002, after 50 years of economic and environmental problems, the mine was taken over in 2008 by Molycorp Minerals Llc, which went bankrupt in 2014[120].

Reopening it, under US environmental protection laws, is impossible. So the processing business is handed over to Chinese companies, which collect the raw material in America, process it in China and then resell it (at a very high price) in the US[121]. Nevertheless, thanks to the rising prices of rare earths, there is now money to be made even in this way[122]. Little compared to the needs that the West will have to face: the world, in which the US used to be the main exporter of fossil fuels, with about 20% of the global supply, is turning into one in which China alone controls more than 75% of all the materials needed for the ecological transition.

There is, however, one topic that can reduce concerns: the recycling of materials, especially in the case of batteries, for which rare earths represent an important share. SiTration, a company at the Massachusetts Institute of Technology (MIT), promises, with the latest technology, to recover more than 95 per cent of the critical materials of which a battery is made, and promises to do so using 10 times less energy than hitherto[123]. The relatively short lifecycle of a lithium battery, currently estimated to be in the order of 10 years, is a negative feature, whereas it becomes an opportunity if it is reused: in this way, most of the materials needed for production would be directly reused, cutting the energy, environmental and geopolitical costs of the supply chain. But if this is true for batteries, it is less true for all other products that have a considerably longer life cycle, such as wind turbines. The only real hope is that technological progress will succeed in replacing current production with less problematic alternative materials.

Is hydrogen the future?

Iberdrola green hydrogen pumping and storage plant in Puertollano, Ciudad Real (Spain)[124]

The replacement of the entire fleet of ICEVs, including hybrids, will take place with EVs powered by lithium-ion batteries: is this the only viable route to an ecological transition? Technology, as we know, runs fast, and often surpasses the imagination. There are many ideas in the pipeline, some at a very advanced stage of realisation. The current competition revolves around hydrogen: it is the most abundant and lightest element in the universe and contains more energy per unit mass than natural gas or petrol, which makes it very attractive for transport. Its oxidation produces a lot of energy and, very interestingly, the only residue of this process is water and other elements with absolutely negligible pollution.

A hydrogen engine is simple to make, resembling a classic heat engine, but has handicaps: poor efficiency and harmful emissions of nitrogen oxides that can react in the lower atmosphere to form ozone, a greenhouse gas. Technology has gone one step further, managing to use hydrogen in an EV: this gas, through its oxidation, is able to generate electricity. To do this, a device called a ‘fuel cell’ is used, which, by the way, exploits an idea that is by no means new: its principle was discovered in 1839 by the English physicist William Grove[125]: these cells replace today’s lithium batteries and that’s it.

Making fuel cells, however, is not very cheap: the weak point is the ‘catalyst’ needed to trigger the chemical processes; at least six different elements belonging to the platinum group – which is very expensive and rare – are used to make it; but even here, research is reaching important milestones: a study published in July 2022 in Nature Energy[126] states that some researchers have managed to make efficient and durable catalysts using less noble metals, such as iron combined with nitrogen and carbon. The product seems to match the qualities of the platinum catalyst, but no longer has its disadvantages[127].

Infinite availability, simple construction, good efficiency (ranging from 40 to 60 per cent), no polluting emissions: do we have the egg of Columbus? Not yet: first of all, hydrogen does not exist free in nature, except in minimal quantities. It occurs bound to other elements such as water or methane, and its extraction requires enormous amounts of energy. The hydrogen currently used as a raw material in industry is produced almost entirely from fossil fuels, resulting in CO2 emissions: it is called ‘grey hydrogen’ when emissions are released into the atmosphere and ‘blue hydrogen’ when carbon emissions are captured and stored. Green’ hydrogen is the only one acceptable within the decarbonisation process: it is extracted from water by electrolysis, but to be called green, the energy to abstract it must be supplied entirely from renewable sources.

But research offers great horizons: a new study from the University of California Santa Cruz shows that hydrogen can be extracted simply and cheaply: using a gallium-aluminium compound to create aluminium nanoparticles, which react rapidly with water at room temperature, producing large quantities of hydrogen and using very little energy. This methodology is currently patent pending and could represent a real breakthrough in the use of hydrogen[128].

Once the problem of extraction has been overcome, there is the problem of storage and transport: hydrogen has a very low density, and storing it means subjecting it to very high pressures (up to 700 bar) or liquefying it, keeping it below -253°C: these activities are also very energy-intensive, the energy cost of liquefaction being about 30% of the fuel’s energy content[129]. Chemical storage is another technology that exploits hydrogen’s ability to bind to chemical compounds or metals, and is extremely effective in reducing its volume by up to 3-4 times compared to other processes, but for the same weight the vehicle has a range three times less than that obtainable with liquid hydrogen or compressed hydrogen with advanced tanks[130]. However, the system is very promising and, as usual, we hope for technological progress.

Due to its very low density, storing and transporting hydrogen creates many obstacles[131]

Distribution is also a particularly costly process: tankers use special, very heavy cylinders, the filling of which requires a lot of energy, and distribution through a pipeline network requires special pipelines with special types of steel and larger diameters, given the high pressures involved[132]. On balance, hydrogen is extremely interesting for its environmentally friendly features, but the process from extraction to its use is still unsatisfactory. There is great excitement in the research universe, and there is hope for a great extension of its application in the near future.

But there are critical voices: a study that appeared in the journal Atmospheric Chemistry and Physics on 19 July this year reveals that hydrogen, when released into the atmosphere, has a far greater ‘heating’ power than previously thought, two to six times greater[133]. Treating hydrogen with extreme caution by paying maximum attention to leakage will therefore be a must: with a 10% leakage rate, a value that many scientists consider plausible, blue hydrogen (with carbon capture and methane loss of 3%) could increase the warming impact by 25% in 20 years. The ‘green’ hydrogen produced would still reduce warming effects by two-thirds compared to fossil fuels, but far less than the climate-neutral promise claimed by hydrogen advocates[134].

The automobile industry has already been involved in producing hydrogen-powered vehicles for twenty years – first with prototypes, then with commercial vehicles: the BMW Hydrogen 7 of 2007 is the first hydrogen-powered car (with a combustion engine) put into circulation in a small series, about a hundred units. Now there are several examples on the market, distributed by the major brands: they have the advantage of an attractive autonomy, since a full tank can be driven for up to 1,000 km, but they are significantly expensive, to the point that some manufacturers offer them for hire. Another major disadvantage are the very few refuelling points: as of today there are only about a hundred in Germany[135], 29 in France[136], 9 in Spain[137] and only 6 in Italy[138]: although general expansion is expected in the short term, we are still very far from sustainable usability.

In heavy mobility, on the other hand, we are already in the midst of fully realised projects: two hydrogen-powered pilot trains, produced by Alston, have already travelled more than 180,000 km in Germany between 2018 and 2020[139], while the first official hydrogen train with fuel-cell batteries started regular service on 25 July this year on the German regional railway line between Cuxhaven and Buxtehude[140]. In shipping there have been realisations as early as 2020, such as the small boat Hydra, the first in the world with a fuel cell engine. Since then, the system has been implemented on various types of ships and submarines, and shows great promise.

The social issue

In the EU, cars on the road are on average 11.8, vans 11.9, trucks 14.1 and buses 12.8 years old[141]

The average age of the car fleet in the European Union is 11.8 years. Lithuania and Romania have the oldest car fleets, with vehicles almost 17 years old; the newest cars are in Luxembourg (6.7 years); the average age of light commercial vehicles is 11.9 years; Italy has the oldest van fleet (13.8 years), followed by Spain (13.3 years); lorries are on average 13.9 years old, Greece has the oldest lorry fleet with an average age of 21.4 years, while the newest are found in Luxembourg (6.7 years) and Austria (7 years); buses are on average 12.8 years old and Greece has the oldest with more than 19 years; only six countries in the European Union have a bus fleet that is less than 10 years old[142].

Looking at the quality and age of the fleets on the road, one can understand the resistance in renewing them, due above all to purchasing power: it is no coincidence that the age of the fleet is almost always inversely proportional to the GDP of the reference area. The average price in Europe of a new car with an internal combustion engine is €32,318, while that of an EV is €42,568[143], with a differential of 31.7%, which, however, varies from region to region (in Italy it is 42%)[144]. The differential worsens if we lower the target: the lowest price of a small-capacity ICEV, again in Italy, is around €10,000 (Dacia Sandero), while the cheapest EV like the Dacia Spring is sold for €20,100[145].

For those with less spending power, buying an EV involves an outlay twice as high as buying an ICEV. The price is expected to fall gradually, mainly due to the decreasing cost of batteries – Volkswagen predicts parity by 2025[146], while BloombergNEF claims they will be even cheaper by then[147] – but the fact remains that for a large segment of the public, buying an EV is a pipe dream today.

With such an ageing fleet, the used car market thrives: 32.7 million used cars were sold in Europe in 202[148] compared to 9,700,192 new cars[149]. In some areas, most car owners commit very little money to their mobility, some out of strategy (second car), most due to poor economic possibilities. With the freeze on the production of ICEVs, those with less spending power will be in great difficulty: the used car fleet, the lifesaver for this category, will be practically non-existent, and the only alternative will be between buying a new vehicle and walking. Freedom of movement, so important, socially, over the last half-century, is in danger of suffering a serious setback.

One has to wonder what dynamics the thermal engine industry will assume during the transition years, i.e. from now until 2035: mechanics and parts manufacturers have to adapt now, abandoning the world of ICEVs. Even refuelling with LPG, petrol or diesel could, at some stage, be a problem, even though the price at the pump will probably be bargain. But the risk is that we will reach the fateful date when a still large fleet of ICEVs survives out of desperate need. The 2035 clear cut could be a guillotine for a large section of society, especially in those countries with a more disadvantaged per capita income. This will force governments to rethink mobility for everyone who needs it: the subsidies offered so far will be irrelevant.

What impact for the automotive industry

Volkswagen ID.3 electric cars on the assembly line[150]

The European Union, with 21% of the world’s car production, is home to the largest car companies and manufacturers in the world: 2.6 million people work in car production, which is 8.5% of total employment in the manufacturing sector, and when the entire supply chain is taken into account, this amounts to 13.8 million people[151]. EVs are mechanically simpler and it is estimated that 30% fewer man-hours are required for their production, i.e. 30% less manpower[152]. Almost all production of the components for ICEVs, which is largely outsourced, will cease and, due to the great diversity of types, manufacturers will have little chance to convert: for those who produce pistons, it is unlikely that they will make sensors or inverters.

If the transition takes place without any preventive measures to cushion the dynamics, about 30 per cent of employment, i.e. more than 4 million jobs, is put at risk. The biggest job losses, however, could be in the supply chain: car companies outsource almost 75 per cent of component production. Moreover, the production process of EVs requires distinctly different skills and professionalism from the workforce. Therefore the risk of forced turnover is real if adequate in-house training is not possible, hence the drama of further job losses.

The Green Deal approach comes at a very delicate stage for the sector: many car manufacturers are already in crisis. In 2020 alone, car sales in the EU fell by 24%, while 844,147 vehicles were sold in March 2022, i.e. 20.5% less than in March 2021 and 51% less than in March 2019[153]; announcements of redundancies are inevitable, including Volvo (which has cut more than 4,000 jobs globally[154]), Renault (around 14,600[155]) and Nissan, which has decided to close its Barcelona factory[156], affecting 3,000 direct jobs and 20,000 indirect jobs (it had lost as many during the 2009 crisis) [157].

One may turn one’s nose up at these arguments set against that of safeguarding the ecosystem, but facts remain facts. Governments and trade unions will have to deal with them. As Winston Churchill said, ‘Never let a good crisis go to waste’: crises pose difficult challenges, but they also conceal new opportunities. It is not only the automotive industry that is losing employment everywhere. Will oil, gas and coal soon become redundant? According to the targets set, it is estimated that at least 60 per cent of fossil fuels will have to be cut within a decade – an impressive quota. How many millions of jobs will be lost? And how will the plants, ports, ships, pipelines, wells be disposed of and cleaned up? Who will pay?

What will happen in the fossil fuel universe?

Soon, the fossil fuel market will undergo a profound change that will reshape the current geopolitical arrangements

According to the EU, the use of coal, the most polluting element in the energy mix, must be substantially reduced by 2030, while oil and natural gas can be phased out later; most of the change for oil and gas will occur between 2030 and 2050. By this time, oil should be almost completely phased out, while natural gas would contribute only a tenth of the EU’s energy in 2050[158]. This is a real revolution.

The path to decarbonisation has been on the road for some time, trying to act on demand suppression with internationally tradable carbon certificates or taxes on CO2 emissions, both of which have pushed governments towards process optimisation and green conversions, often using public incentives. But all this has not helped. The demand for coal is constantly increasing, especially in developing countries that are growing industrially at a very fast pace.

Currently, energy demand is back to pre-pandemic levels. According to an analysis by BP, more will be used in 2021, considering the surge in demand – the most impressive in human history; at the same time, emissions have also returned to previous levels[159], as BP explains: ‘Significant progress has been made on sovereign commitments to achieve net zero, but these growing ambitions have yet to translate into tangible progress on the ground. The world remains on an unsustainable path”[160].

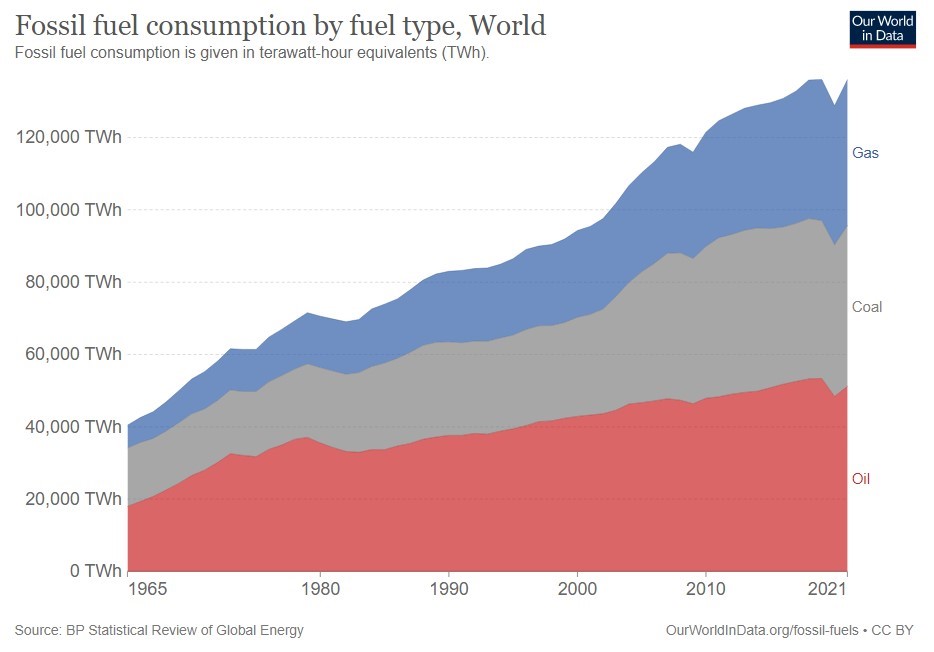

Global fossil fuel consumption by type[161]

Yet at least 13% of the energy produced in 2021 relied on renewable sources, a 17% increase over the previous year: the problem is that the use of fossil fuels remains very high[162]. In freight transport, a sector responsible for 14% of greenhouse gas emissions[163], the dynamics are not so different: with the Covid-19 crisis, global demand for oil fell by 57% in the early 2020s and then rebounded in 2021, so that consumption is just 3% below pre-Covid-19 levels again[164], but this is only because the aviation sector has a slower recovery[165].

According to the IEA, we will see a steady growth in demand for fossil fuels for global use until at least 2025, when a turnaround will begin: under the assumed scenario, oil demand will peak just after 2025 (97 million barrels per day) and then fall by about 1 million barrels per day per year until 2050, but only if current climate commitments are fully met; otherwise, in the most pessimistic forecasts, the turnaround could be in 2050[166]. Even in the most optimistic scenario, 77 million barrels per day will still be consumed worldwide in 2050 – less than the current 100 million barrels per day, but still too many[167]. Not an easy situation for those who aim to achieve the coveted ‘net zero’ climate change emissions by 2050.

To achieve this we would have to drop to 25 million barrels per day by 2050[168]. An outcome that appears impossible. According to the IEA, current climate commitments would only lead to one-fifth of the emission reductions by 2030, and achieving this target would require investments in clean energy projects and infrastructure of more than three times the financial allocations of the next decade, while spending on clean energy is far below what would be needed[169].

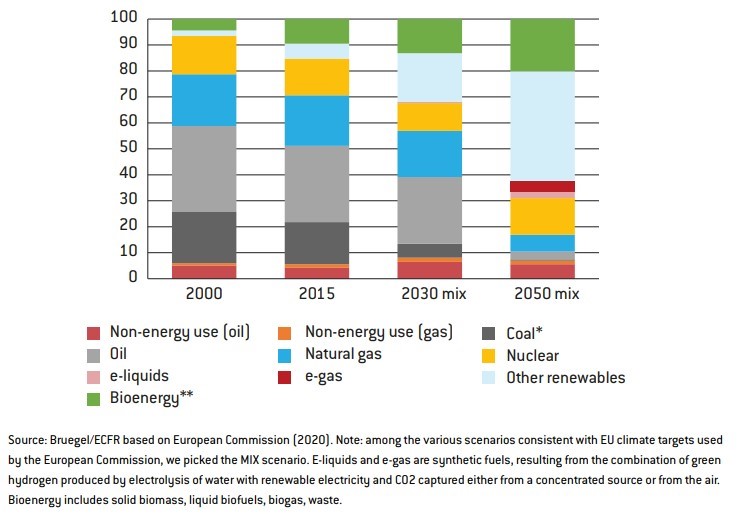

Evolution of the energy mix in the EU (-55% emissions in 2030 compared to 1990 and climate neutrality in 2050)[170]

These disappointing prospects are confirmed by the OECD: government support for fossil fuels, in 51 countries worldwide, has almost doubled to USD 697.2 billion in 2021, from USD 362.4 billion in 2020, due to rising energy prices on a global scale, and the trend will continue for at least the whole of 2022[171]. Hard times for decarbonisation, which is at least postponed until after the resolution of the conflict between Russia and Ukraine.

For every three barrels of oil consumed worldwide, two are absorbed by the transport sector[172]. It is undeniable that the European Green Deal will have profound repercussions, influence geopolitics through its impact on the EU’s energy balance and global markets, oil and gas producing countries, European energy security, and global trade patterns, especially with regard to the border carbon adjustment mechanism[173]. The likely scenarios are all to the detriment of exporting countries: Europe’s exit from fossil fuel dependence, with its market representing 20% of the world’s, will negatively affect a number of regional partners who may face economic and political destabilisation. Such a major drop in demand will also affect the rest of the market by depressing prices. Will fossil fuel producers and exporters passively accept this transformation?

In the case of oil, the main producers to date are the United States, Saudi Arabia and Russia, which produced around 40 million barrels of oil per day in 2020 alone, or 43% of world production[174]. From a global perspective, according to a recent analysis by the Department of Mechanical Engineering of the University of Antwerp, the fossil fuel market is capable of generating profits of almost $3 billion per day; oil companies have earned $52 trillion (billion) since 1970 with an average annual profit of over $1 trillion[175]. One observes that a market with this immense availability of wealth is easily able to protect itself: nations such as Russia, like those in the OPEC cartel, are able to steer the markets to their own advantage and thus curb the development of renewables[176].

In the US, there is a war on decarbonisation: in November last year, Republican state treasurers gathered at a conference organised by the State Financial Officers Foundation (a small non-profit organisation based in Kansas with close ties to fossil fuel lobbyists[177]) in Orlando, Florida, to create a real shield of protection for fossil fuel companies[178]. Riley Moore, the treasurer of West Virginia, has excluded several large banks, including Goldman Sachs, JPMorgan and Wells Fargo from government contracts with his state because they are reducing their investments in coal[179]. Also, Moore and the treasurers of Louisiana and Arkansas have withdrawn more than $700 million from BlackRock, the world’s largest investment manager, objecting that the company is too active on environmental issues[180]; at the same time, the treasurers of Utah and Idaho are pressuring the private sector to abandon climate action[181].

A huge legal granola is also looming: foreign investments are regulated by thousands of international investment agreements, which include investor-state dispute settlement provisions[182]. The European Union is a signatory to the ECT, the Energy Charter Treaty, an agreement that allows foreign investors to seek financial compensation from governments if changes in energy policy adversely affect their investments: a formidable brake on the Green Deal, calling its foundations into question[183].

Recently, there has been a blossoming of disputes between investors and states on the basis of bilateral or multilateral investment treaties: the investment arbitration cases against the Netherlands due to the Dutch government’s decision to phase out coal-fired power plants (RWE vs. Netherlands , ICSID Case No. ARB/21/4 ; Uniper vs. Netherlands , ICSID Case No. ARB/21/22) and a case brought against Italy’s refusal of a coastal drilling concession (Rockhopper vs. Italy , ICSID Case No. ARB/17/14)[184]. In March 2021, the German government settled a dispute with a number of companies (Vattenfall, RWE, E.ON and EnBW) for forcing them to shut down their nuclear power plants prematurely in response to the Fukushima disaster: the total compensation, after years of litigation, was USD 3.1 billion[185].

Similarly, various stakeholders have filed claims worth $15 billion against the US for the cancellation of the Keystone XL pipeline project[186]. A study published by Science on 5 May 2022, estimates that governments’ actions to limit fossil fuels could trigger claims of up to $340 billion from investors in the oil and gas sector alone: a staggering amount that, when broken down by country, for some could even exceed national GDP[187], especially in the global south[188].

This figure, according to the author, Kyla Tienhaara[189], is a conservative estimate, as it does not include coal industry projects[190]. Such disputes can thus become a powerful tool in the hands of the fossil industry to slow down if not totally block, especially in some economically disadvantaged countries, the decarbonisation process[191]. In any case, the transition, geopolitically speaking, will not be smooth, especially given the tense relations with Russia and China. EU foreign policy will be crucial to avert crises that may undermine the goals of the Green Deal. The EU and its oil and gas exporting neighbours have time to plan properly for this transition. Until 2030 we will continue to import oil and gas – the real decline will only begin after that.

A different mobility

The backbone of the Trans European Network Transport, born in 1993 and relaunched by the Green deal policies[192]

On 14 December 2021, the European Community publishes a transport proposal[193] with the aim of harmonising the needs of the market with those of the European green deal: a ) it offers to increase connectivity and move more passengers and goods by rail and inland waterways (revitalisation of the TEN-T axis), as this is currently the safest route with the lowest pollutant emissions; b) it promises to boost long-distance and cross-border rail traffic: only 7% of the kilometres travelled by train between 2001 and 2018 involved cross-border journeys; there will be easier, cheaper tickets, tax incentives; c) it looks at the needs of drivers with the improvement of infrastructure (among them the drastic increase of refuelling stations for EVs) and the encouragement of digital, making more and more crucial traffic data information available in real time.

But it is the part on urban mobility that is the most interesting[194]: the points touched upon aim to solve the growing congestion in city areas – 23% of all transport-related greenhouse gas emissions are generated in cities – through a complex plan that aims to make urban transport resilient, environmentally friendly and energy efficient – by identifying zero-emission solutions for urban logistics, promoting active travel (on foot or by bicycle), incentivising zero-emission urban transport and car sharing. Suffice it to think of the German experiment where this year, for three months, a single fare of €9.00 applied to all national public transport was adopted: 52 million tickets were sold as of the end of May, 42 million more than in the same period of the previous year, and this translated into 1.8 million tonnes of CO2 saved in three months[195].

These proposals, it says, ‘will put the transport sector on track to reduce its emissions by 90 per cent’[196]. A well-crafted plan, which lacks a fundamental part: a concrete idea that discourages travel. In Italy, for example, 67.9 per cent of people travel daily for work – a very high percentage[197]; in Germany at least 3.4 million people travel daily from one federal state to another for professional reasons[198]. Everywhere in Europe, if you look at the statistics, both public and private transport is mainly used for work purposes.

During the lockdowns that were resorted to because of the pandemic, cities all over the world had to relate to their professional environments in a completely different way, and the move to teleworking underwent an unprecedented increase. Efficiency has increased and costs have been reduced. Employees have improved their quality of life: no more commuting and finding a parking space. Most of all, the environment has benefited: drastic reductions in energy consumption, city traffic, emissions and kilometres travelled. We would have liked more courage from the European Commission in this regard: a detailed plan, incentives for the various countries to adopt the right legislation, awareness campaigns.

What sustainability?

Pollution-free streets of Seoul following months of pandemic[199]

This work of ours concludes with one certainty and many questions. The certainty is that pollution from fossil fuels is responsible for abrupt climate change and that, because of this, there is widespread agreement that environmental issues should be tackled with the belief that time is a tyrant. But such decisions can have particularly insidious domino effects, which risk undermining objectives and even having counterproductive effects on sustainability.

The serious environmental damage, child exploitation and inhuman conditions of mine workers will be exacerbated by the soaring demand for minerals; the problem of disposal processes risks spiralling out of control and becoming largely unsustainable; the rethinking of infrastructures related to electricity distribution, energy sustainability itself at source (the current crisis is forcing a u-turn in the direction of fossil fuels) takes on titanic proportions; the consequences in terms of electromagnetic pollution, hitherto largely underestimated, risk turning into a serious boomerang; closing the door in the face of oil-producing countries could trigger serious destabilisation; a large part of western families could be faced with unsustainable costs and be prevented from moving, and tourism could be seriously affected; there will be, in Europe alone, millions of unemployed, banks in difficulty, industrial sectors that will lose know-how or go out of business. And we will not have sufficient energy sources, and even if we do, it will be the distribution network that will be totally inadequate – all questions to which no one seems to have sought answers.

There is a growing certainty that the death sentence pronounced against the combustion engine is a reckless leap in the dark, and seems to have been pronounced by a pool of executors seriously lacking the capacity to understand their own act. Industries are preparing: they are turning assembly lines and making redundancies. What will we do if we realise halfway through that we cannot meet the targets? Why does Brussels not care? What is the real sustainability of the whole project? Is it really a project, or a crazy decision made on a day of gloomy mood?

The European Green Deal remains an important response to the challenges facing the world and Europe, but we would like a little more realism and caution. We aim to make Europe the first climate-neutral continent by 2050, but we demand clarity on too many aspects that are completely ignored. Transforming the economy into a clean and circular system, reducing pollution and restoring biodiversity, is no longer a choice, but an obligation to work together – it is the only way to try to reverse a destructive process that is expressing its full force with climate change. But a planet is not saved by the blindness of the interstellar bureaucracy of Douglas Adams’ dystopia.

It is a fight against time, and we do not have much of it left.

[1] https://evspias.com/the-european-parliament-approves-the-end-of-combustion-cars-in-2035/

[2] https://www.consilium.europa.eu/en/policies/green-deal/fit-for-55-the-eu-plan-for-a-green-transition/

[3] https://oeil.secure.europarl.europa.eu/oeil/popups/summary.do?id=1706841&t=e&l=en

[4] https://pledgetimes.com/stop-thermal-car-sales-germany-says-no/

[5] https://www.bloomberg.com/news/articles/2021-07-12/france-pushes-back-against-eu-banning-combustion-cars-by-2035#:~:text=France%20is%20resisting%20the%20European,for%20plug%2Din%20hybrid%20models.

[6] https://www.repubblica.it/economia/2022/06/09/news/cingolani_partiti_divisi_sulla_frenata_alle_auto_elettriche_i_verdi_e_il_ministro_delle_fonti_fossili_tajani_bene_s-353144542/

[8] https://www.wallstreetitalia.com/lue-mette-al-bando-auto-a-diesel-e-benzina-a-partire-dal-2035-anfia-a-rischio-70-mila-posti-di-lavoro/#:~:text=%E2%80%9CSono%2070.000%20i%20posti%20di,di%20ricarica%20o%20altri%20componenti.

[9] https://www.repubblica.it/economia/2022/06/09/news/cingolani_partiti_divisi_sulla_frenata_alle_auto_elettriche_i_verdi_e_il_ministro_delle_fonti_fossili_tajani_bene_s-353144542/

[10] https://www.reuters.com/markets/europe/five-countries-seek-delay-eu-fossil-fuel-car-phase-out-document-2022-06-24/#main-content

[11] https://www.world-today-news.com/economica-net-problems-inside-acea-worsen-after-stellantis-volvo-leaves-the-association/

[12] https://newsbeezer.com/hungaryeng/another-car-manufacturer-leaves-the-association-of-european-car-manufacturers-in-shards/

[13] https://www.eceee.org/all-news/news/factbox-fossil-fuel-based-vehicle-bans-across-the-world/

[14] https://www.eceee.org/all-news/news/factbox-fossil-fuel-based-vehicle-bans-across-the-world/

[15] https://news.trust.org/item/20201204160932-5143z/

[16] https://www.virta.global/en/global-electric-vehicle-market?__hstc=51530422.19d2ccb43c194831416b184713b74aeb.1658419090585.1658419090585.1658419090585.1&__hssc=51530422.1.1658419090585&__hsfp=3543246309&hsutk=19d2ccb43c194831416b184713b74aeb&contentType=standard-page&pageId=11330961497#nine

[17] https://www.virta.global/en/global-electric-vehicle-market

[18] https://www.virta.global/en/global-electric-vehicle-market?__hstc=51530422.19d2ccb43c194831416b184713b74aeb.1658419090585.1658419090585.1658419090585.1&__hssc=51530422.1.1658419090585&__hsfp=3543246309&hsutk=19d2ccb43c194831416b184713b74aeb&contentType=standard-page&pageId=11330961497#nine

[19] https://www.iea.org/data-and-statistics/data-product/global-ev-outlook-2022#

[20] https://www.news18.com/news/auto/4-2-million-evs-sold-in-first-half-of-2022-globally-china-leads-5746459.html

[21] https://seekingalpha.com/article/4528473-ev-company-news-month-july-2022

[22] https://www.iea.org/data-and-statistics/data-product/global-ev-outlook-2022#

[23] https://www.iea.org/reports/global-ev-outlook-2022/executive-summary